With AEP just over 100 days away, here are the latest enrollment trends for the MA market.

We're seeing structural shift in how carriers are assessing their markets. Agents who understand it will have a real advantage heading into the fall.

The market is changing

Several major national carriers saw net enrollment losses during AEP and OEP. At the same time, new opportunities continue to emerge:

- MA enrollment has gained nearly 1 million new members from January to June, representing 3% growth.

- The fastest-growing segments are C-SNPs and giveback plans. Giveback enrollments grew 7.4%, while C-SNP enrollments grew 11% since January.

- Emerging carriers like Devoted, SCAN, and Alignment are stepping in where national carriers are pulling back.

.png)

.png)

.png)

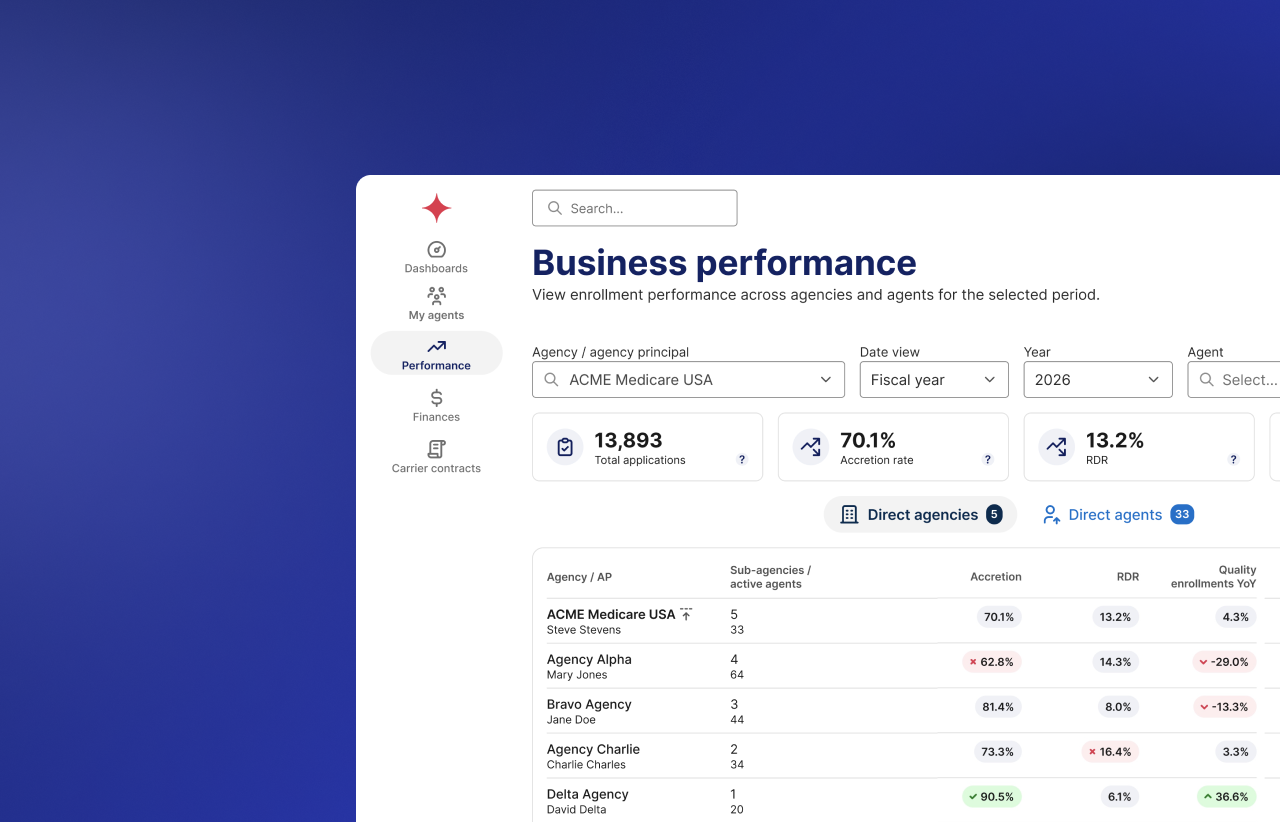

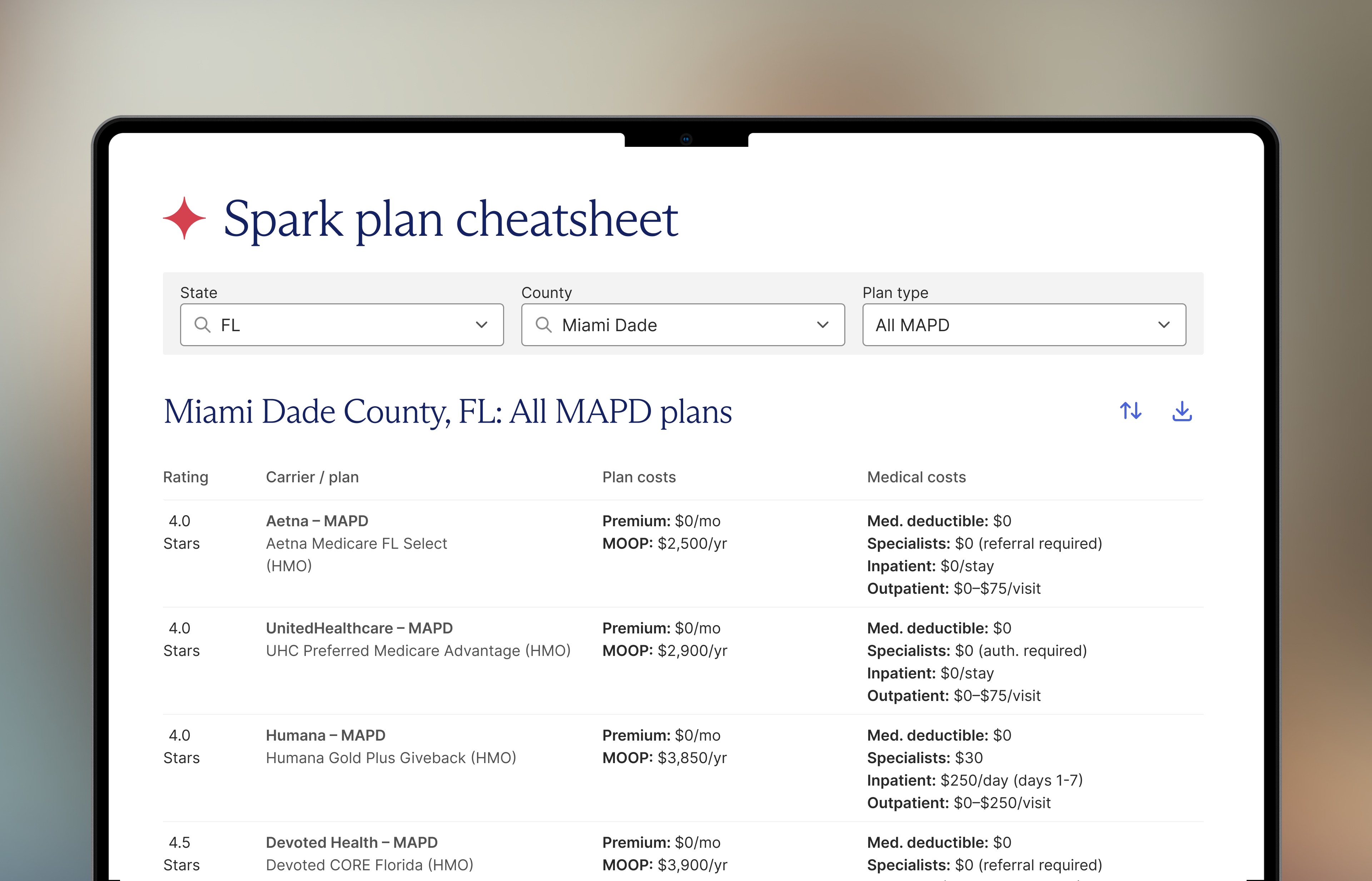

Carrier mix recommendations

This year, a winning shelf looks different: anchor carriers for volume and breadth, emerging carriers for specific growth markets, and category coverage (giveback, C-SNP, D-SNP, core HMO/PPO) to meet the full range of what clients need. Our recommendations:

.png)

Aim for 6-8 contracts across these categories to ensure a diverse mix and depth.

- Anchor carriers provide volume, name recognition, and the ability to hold your existing book. Humana (+360K net growth), Aetna (+80K), and UHC (despite its net decline) remain essential because of their scale and the clients already enrolled in their plans.

- Emerging carriers to round out the lineup for specific geographies and high-growth segments. Take a look at Devoted, SCAN, and Alignment.

- Category coverage ensures you're equipped regardless of what a client needs: at least one strong giveback plan, C-SNP depth, D-SNP access where relevant, and core HMO/PPO options for volume.

Review your contracts now and identify any gaps in your lineup. The agents who show up to AEP 2027 with the right shelf will have a real edge.

.jpeg)

%201.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpeg)