We founded Spark because we recognized Medicare Advantage's essential value to beneficiaries and the pivotal role agents and agencies play in advising their clients on crucial health decisions. We love MA, and we love Medicare agents.

CMS rightly identified structural problems that were beginning to threaten the MA program's ability to achieve its original aims. Their latest solution, published in the 2025 Final Rule, will require adjustment for the entire industry, but we believe it will set a stronger foundation for the future by pressuring all industry participants to get better.

We are really excited at Spark. This is our opportunity.

There are lots of changes happening in MA, but for this post we will focus on our corner of the industry: the brokers.

What does this mean for brokers?

The greatest enemy to independent MA brokers isn’t CMS – it’s a small number of bad actors, including many FMOs, who abused the prior compensation system into ballooning costs through excessive “administrative payments” and payments to FMOs as carriers. CMS correctly labeled this dynamic as a “bidding war” where FMOs played carriers off each other to maximize compensation while misaligning broker incentives.

To address this issue, CMS explicitly states three priorities. Quoting from the rule:

- Generally prohibit contract terms between MA organizations and agents, brokers, or other TMPOs that may interfere with the agent’s or broker’s ability to objectively assess and recommend the plan which best fits a beneficiary’s health care needs

- Set a single agent and broker compensation rate for all plans, while revising the scope of what is considered ‘‘compensation”

- Eliminate the regulatory framework which currently allows for separate payment to agents and brokers for administrative services.

In short, CMS is prohibiting broker compensation structures that prevent the broker from making objective plan recommendations. We believe this is important and necessary for a well-functioning distribution system. This means administrative payments like HRAs to brokers are prohibited and replaced with a $100 in Y1 and $50 increase in renewal FMV compensation. Leads, marketing co-op, or other payments-in-kind to brokers for enrollments are likely also prohibited.

What does this mean for FMOs?

Importantly, CMS explicitly writes that the all-in single compensation rate and prohibitions on additional administrative payments do not apply to FMOs: FMOs can continue earning commission overrides and other revenue streams from carriers.

This clarification is important, and it is good news: it means CMS recognizes the infrastructure role FMOs play in supporting independent brokers, a function each carrier would have to re-build individually if FMOs went away.

However, MA organizations are prohibited from entering contracts with FMOs that may inhibit their affiliated brokers’ ability to make objective plan recommendations. CMS provides several examples of such contract terms we’ve seen in our day-to-day:

- FMO compensation or reimbursement rates contingent on meeting specified enrollment quotas

- Bonuses paid with the explicit or implicit understanding that money will be passed on to agents or brokers based on enrollment volume

- Providing leads or other incentives based on enrollments

CMS is providing carriers broad direction on the types of incentives to be avoided without being “overly prescriptive” on how they should structure their agreements. CMS will use a “reasonableness standard” when evaluating carrier agreements, and it will revisit FMO practices in rule-making for 2026 and beyond. This is our opportunity to self-regulate.

What next?

It’s now on the carriers to decide how they will implement this rule. We don’t know yet how things will shake out, but if we had our way, we would encourage carriers to use this opportunity to rethink their FMO relationships with a focus on value.

Many FMOs have been overpaid for a very long time, and this has led to an industry unfortunately more focused on horse-trading than delivering value: FMOs negotiate volume-based incentives from a carrier, then use those incentives to recruit additional agencies under them with little attention applied to the broker actually doing the work. This dance is not sustainable.

Providing table-stakes contracting or administrative services should no longer be enough to justify FMO pay. With volume-based compensation under scrutiny, carriers should evaluate FMOs on their ability to deliver real business outcomes to agents and back to the carriers themselves.

Life is getting harder for brokers with growing plan complexity, increased compliance requirements, and changing consumer behaviors amid a turbulent MA market. To justify their keep, FMOs should provide real technology and services that drive not just enrollment growth, but higher retention, lower disenrollment rates, improved member satisfaction, the list goes on.

It’s time to expect more from FMOs

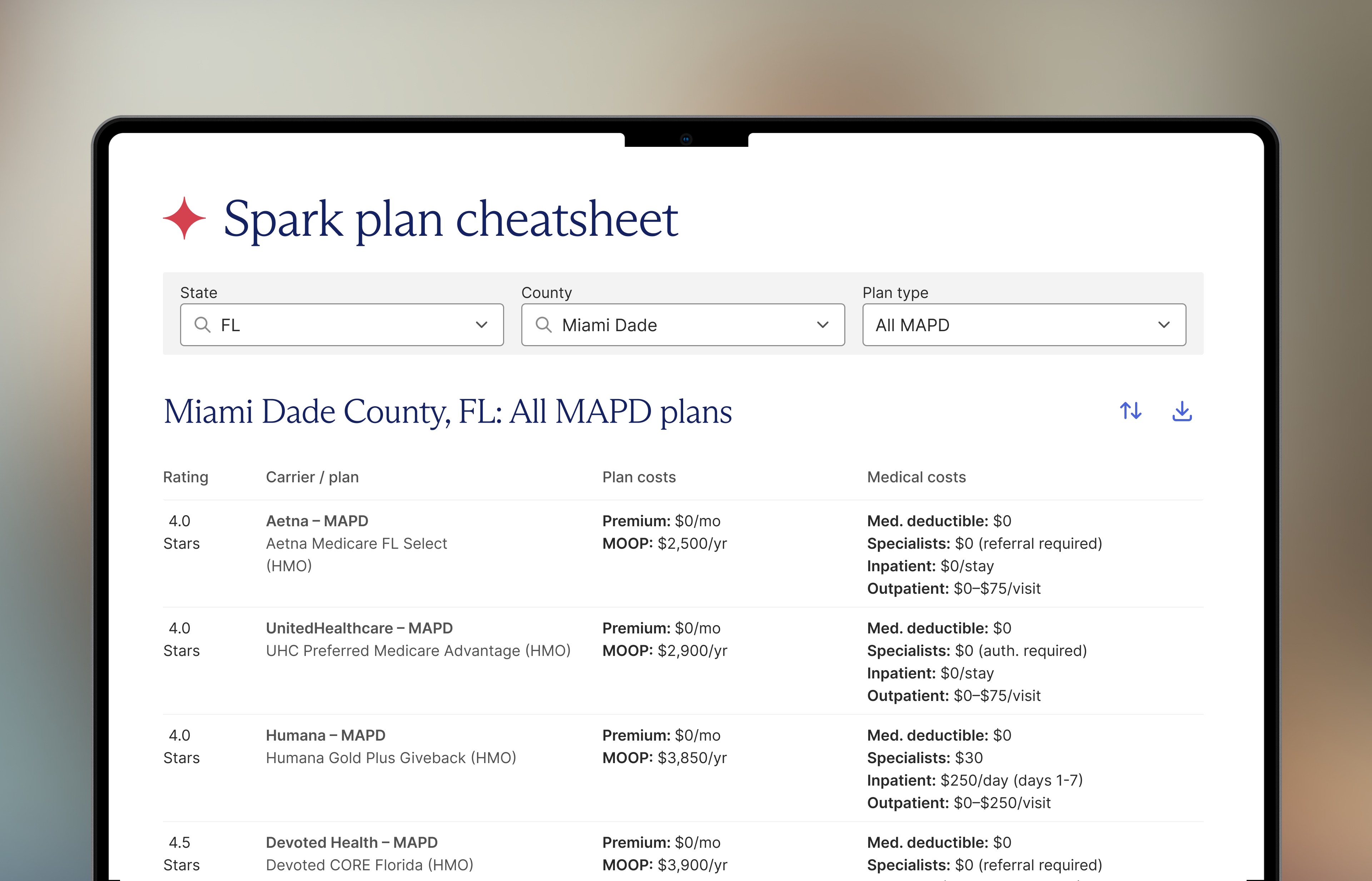

From day one, Spark has been focused on delivering unbelievable value to brokers. We built a home-grown technology platform made just for independent brokers and agency owners that puts all workflows in one place – from marketing to CRM, customer service to commission management, contracting to compliance – streamlining the disparate workflows brokers deal with today.

We’re the only scaled FMO that offers client support to a broker’s entire book of business, helping over 130,000 clients deal with issues like provider search & scheduling, medical bill advocacy, Medicaid certifications, and more. We’ve streamlined byzantine contracting processes with technology, onboarding over 4,000 brokers in 3 years and processing 60,000 contracts in 2023 alone – saving our partners 400,000 hours while helping brokers get contracted more quickly. In 2023, we helped over 3,000 broker partners grow their enrollment volume over 50% while maintaining a 96% client satisfaction rate.

FMOs play an essential role in keeping the MA machine going. It’s time to take that role seriously.

It always ends with the broker

Through all its rulings, CMS noticeably never questioned the special role of the broker. We continue to be in awe at how a $400Bn industry is held on the backs of independent, largely mom-and-pop brokers who deeply care about their clients and communities. We’ve always recognized the large role brokers play in the entire member journey – as sales agent, but also trusted advisor, navigator, and advocate.

We hope that these changes refocus the industry away from horse-trading and toward value: fix the broken incentives, and in the process help the best brokers do even more for their clients.

%201.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpeg)