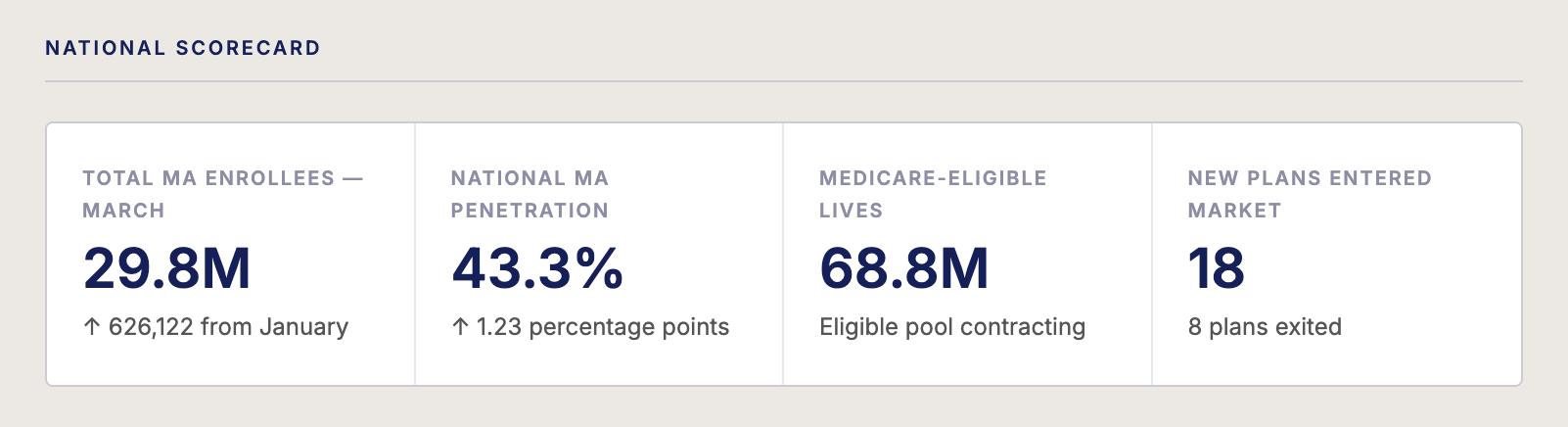

The individual Medicare Advantage market added more than 625,000 net new members in February and March. Total individual MA enrollment now sits just under 30 million, with penetration at 43.32%.

Where did the growth come from?

Plan exit SEPs helped fuel early year growth

Members whose plans weren’t renewed for 2026 had to go somewhere. Some tested the waters with a Supplement or Original Medicare, but the data shows many have made their way back into MA. The plan exit SEP window created real churn — and real opportunity for agents who were paying attention.

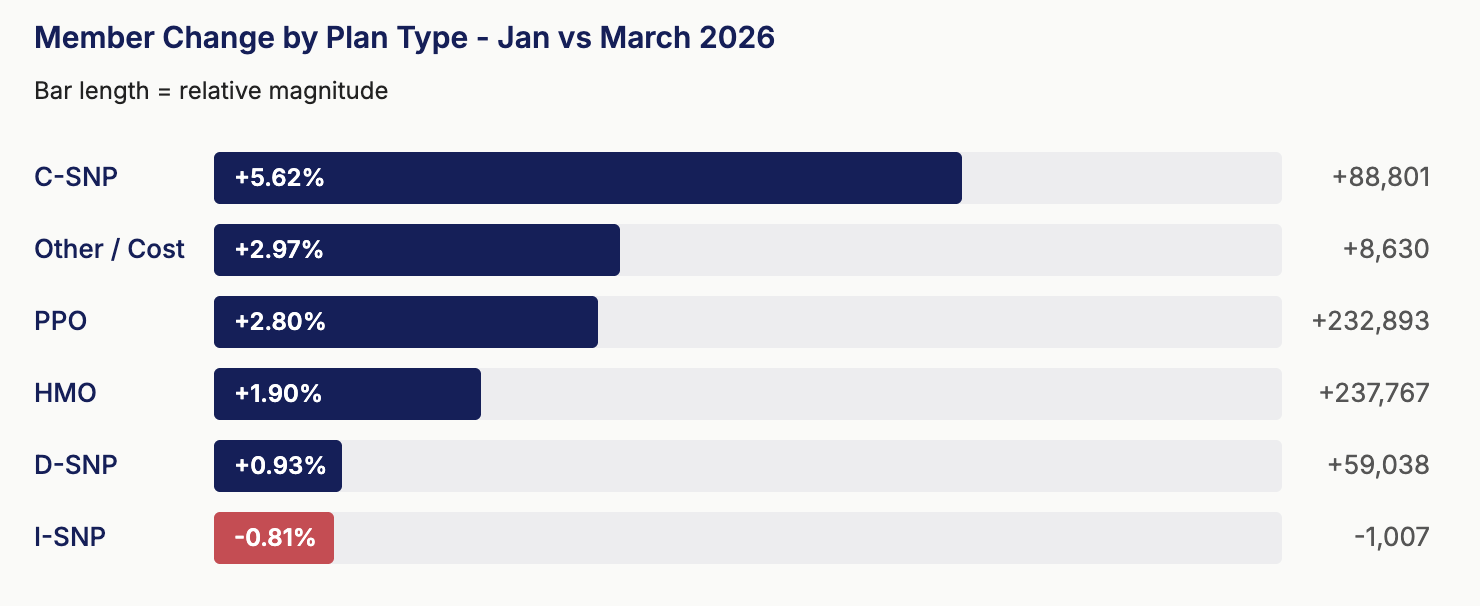

C-SNPs are the fastest-growing segment

C-SNPs are growing at six times the rate of D-SNPs right now. In just two months, the segment added nearly 90,000 new enrollees.

That’s not a coincidence. Carriers have been investing in chronic condition populations, and members who land in the right C-SNP tend to stay. Retention is structurally better when a plan is actually designed for someone’s needs, rather than just being the lowest-cost option at AEP. If C-SNPs aren’t part of your current marketing, that’s worth revisiting.

D-SNPs continue to gain ground

D-SNP is the largest SNP segment at 6.4 million members, but it only grew 0.93% over the same two months. That’s the slowest of any SNP type.

The gap between size and growth rate points to something real: dual-eligible beneficiaries are harder to reach through traditional channels. The agents closing that gap tend to be the ones building community presence and bilingual capabilities — not running the same playbook they use for standard MA.

Illinois led the country in D-SNP growth in February and March, up more than 10% as the new integrated program continues to take hold. Ohio, Michigan, Pennsylvania, North Carolina, and several other states have all posted meaningful D-SNP gains since January. If you’re licensed in any of these states and have dual-eligible clients in your pipeline, the market is moving.

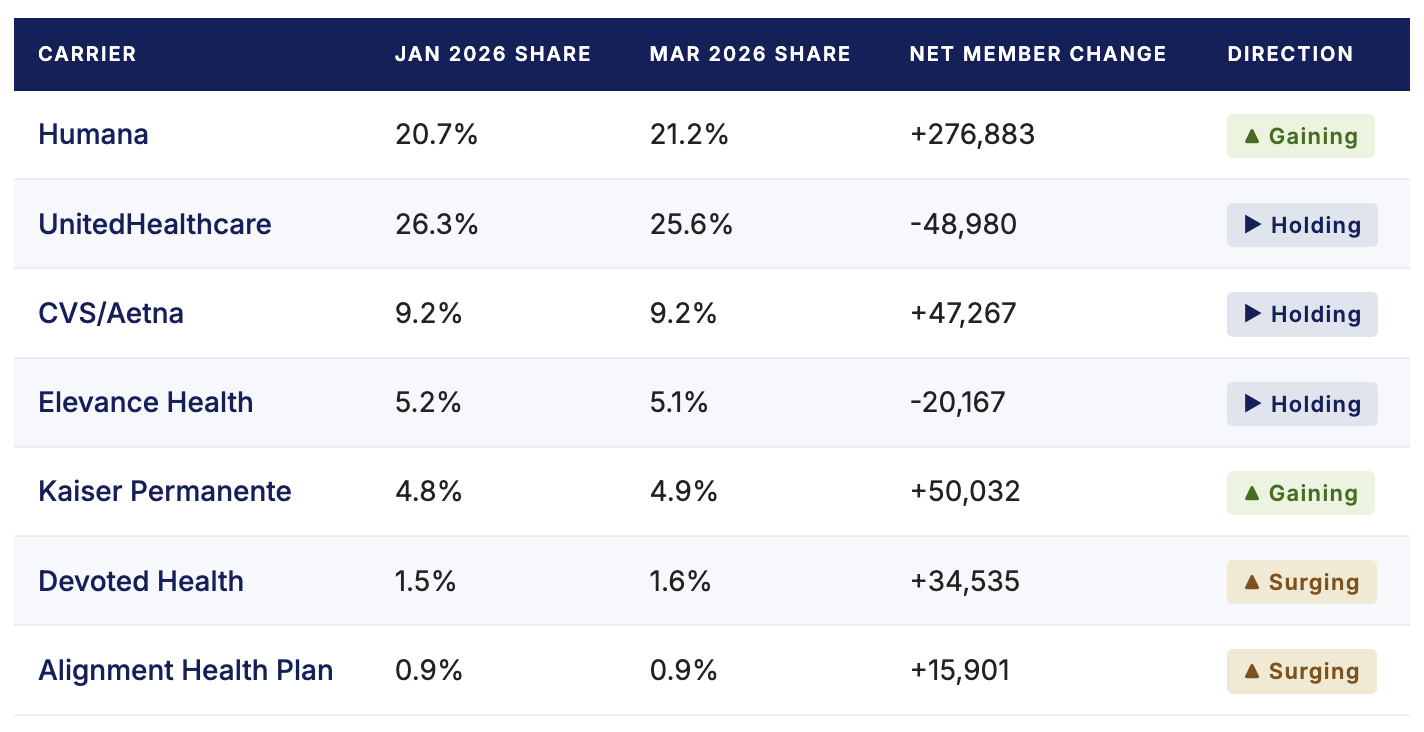

Revisit your carrier mix

Humana had a strong February and March, adding nearly 280,000 members and now holds 21.2% of the individual Medicare Advantage market share nationally. UnitedHealth shed close to another 50,000 members. Elevance Health, Wellcare, and Florida Blue also lost ground in the OEP.

Outside the majors, Devoted Health, Alignment Healthcare, and Kaiser all posted standout growth. These are value-based care models, and better clinical outcomes mean lower disenrollment - which compounds over time. Their growth isn’t random.

The practical question for agents: where is your book concentrated? Carriers losing membership are under pressure, and that pressure tends to surface in service, benefits and pricing before you see it in renewals. If a meaningful share of your book sits with shrinking carriers, now is a good time to think through your exposure and strategize on how to grow with additional carriers.

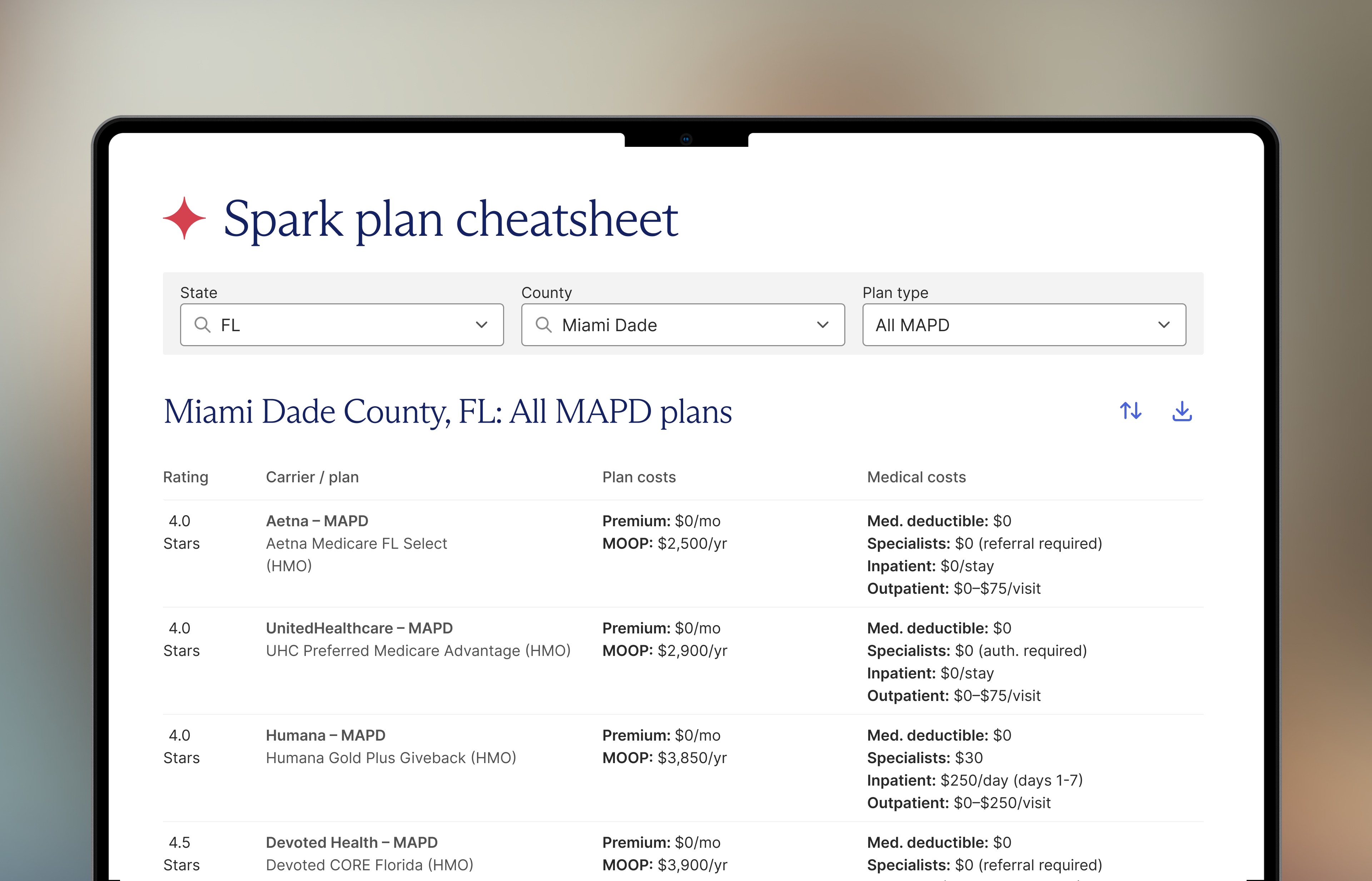

Check out this snapshot for additional county-level insights and compliance best practices. The agents winning in2027 are the ones refining their carrier diversification targets, SNP production plans, and operational workflows.

.jpeg)

%201.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpeg)