Medicarians 2026 brought together the largest gathering of Medicare distribution professionals in the country. Over three days at the Fontainebleau in Las Vegas, the Spark team attended sessions, hosted partners, and had hundreds of conversations on the floor.

What we heard regarding carrier quality, retention, and the trends below wasn't new to us. It's what we've been talking about and building towards with agency owners for the past two years. But hearing carriers, health plans, FMOs, and top agents discuss these topics made it clear that our roadmap isn't a fringe perspective anymore: this is where the industry is going.

Here are five trends that kept surfacing.

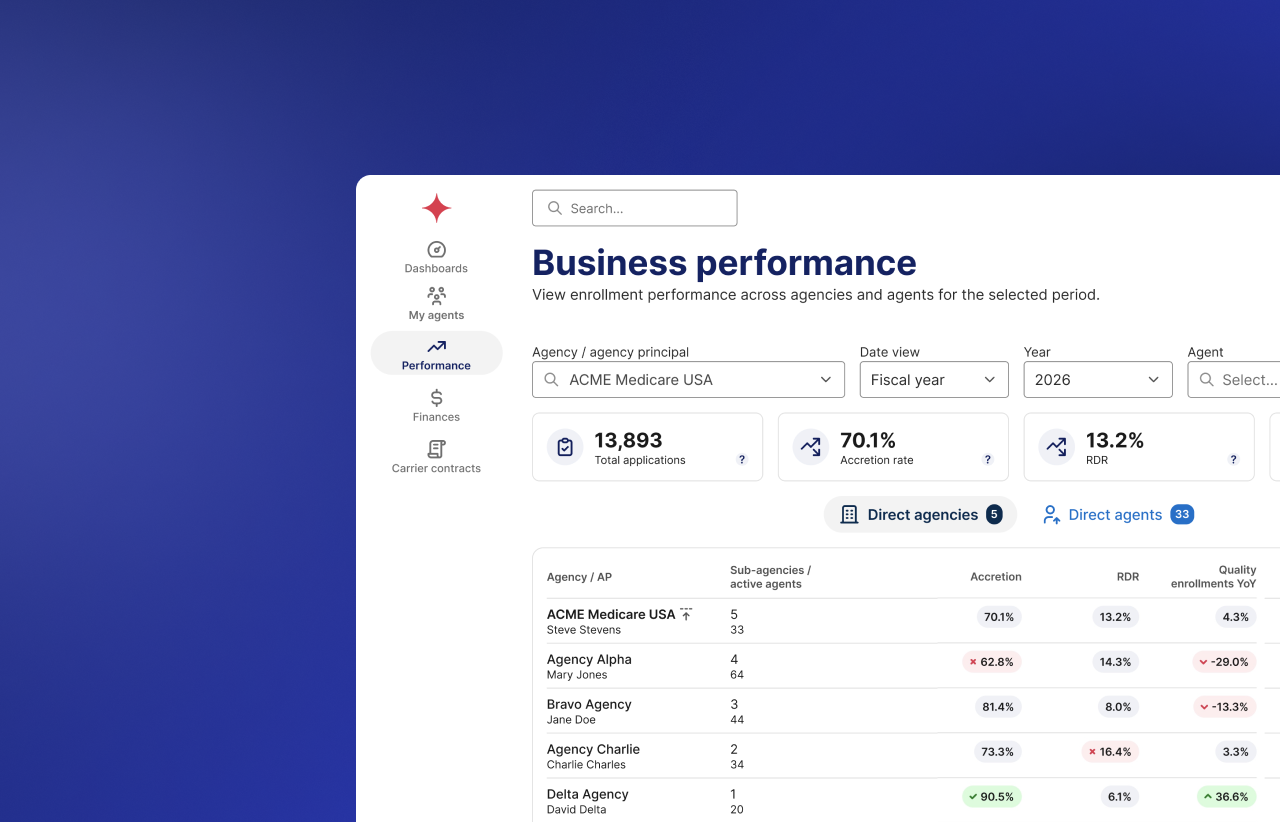

Carrier priorities have shifted from volume to quality

The sessions this year weren't about growth targets. They were about what happens after enrollment. Carriers are paying attention to accretion rates, CAHPS scores, and retention numbers. They're asking whether the enrollments coming through your agency are the right fit and whether members are actually staying.

The shift is structural. Benefits have gotten leaner and plan choices have gotten more complex. Carriers can no longer absorb bad enrollments and expect the math to work. The broker who does a genuine needs assessment and puts clients in the right plan is becoming a competitive advantage for carriers, not just for clients.

"The pendulum has shifted back toward quality. It's all about the client's experience. What that experience needs to become is getting matched with the best possible plan for them, unlocking their best possible health. And that's where everybody in this room plays a pivotal role." – Nick Tatge, Spark

Spark's CEO James Jiang discussed this pendulum swing in his panel discussion:

Retention is the real growth lever

If you're still measuring success by new enrollments alone, you're measuring the wrong thing. The agencies pulling ahead right now built retention systems before they needed them. Every client you keep is one you don't have to replace. Every satisfied client is a referral waiting to happen.

The mechanics are straightforward: systematic touchpoints, anniversary reviews, proactive outreach during plan change season. What's not straightforward is building the infrastructure to do that at scale across your whole book. The agencies that have a system aren't doing more work.

"Phase 1 is retention. Phase 2 is referrals. And we only ask for referrals when a client says 'what can I do to pay you back?' That's when we say: my services are free, but tell your friends and family about me." – Sandra Ochoa, Vemax Insurance Agency

Check out this discussion on fostering customer loyalty, led by our Head of Sales Caleb Campbell:

Be strategic about which carriers you partner with

The past two AEPs taught a painful lesson about carrier dependency. Agents who built their books on a single carrier and watched it exit their market felt that in a real way. The conversation at Medicarians wasn't just about diversifying for risk's sake. It was about choosing carrier partners the same way you'd choose any business partner.

Do they communicate transparently when disruption is coming? Do they protect your book when they make changes? Do they treat you as a partner or as a distribution channel? The carriers worth your loyalty are the ones who earn it.

"Choose your health plan partners carefully. Is the health plan truly partnering with you? Are they giving you advance notice when there's going to be disruption? Or are they just asking more and more and more of you?" – Jen Cohen-Smith, Healthfirst

Ancillary products are the biggest untapped opportunity in your existing book

Less than 1% of Medicare agencies actively cross-sell ancillary products. That number came up more than once this week. And every time it did, the reaction was the same: why aren't more of us doing this?

Hospital indemnity, dental, final expense aren't add-ons — they're gaps your clients already have. You've built the trust and have the relationship to take advantage of the opportunity sitting in your existing book right now. Here are the carriers that Spark supports.

“Stop leading with the $0 premium. Do a fact finder. Ask about investments, life insurance, income — get the full picture. When you do that, you cross-sell naturally, you build a real relationship, and you actually get remembered. It's not a transaction." – Dustin VanDuine, Rick Young Insurance

"Hospital indemnity is literally on the scope of appointment. CMS put it there on purpose — they're telling you to present it. They want you to do right by the member. We're just not listening." – Caleb Campbell, Spark

Our Head of Life & Ancillary Jesse Hendon dove into how brokers can expand beyond Medicare:

The broker identity shift: from enrollment machine to healthcare advisor

The broker whose entire value prop is getting someone signed up has a problem. With CMS expanding digital enrollment, carriers building direct-to-consumer tools, and AI getting better at matching people to plans, the transactional piece of this job is getting automated.

What isn't getting automated is the relationship. The agent who calls when a plan exits the market, who catches that a client's PCP just left the network, who knows enough about a client's health situation to say, "That plan isn't right for you." That's not an enrollment machine — that's a healthcare advisor. And that's a role no algorithm is going to replace.

The agents who are building durable businesses right now have made the shift. They're not just selling plans during AEP. They're the person their clients call year-round. That changes your retention, your referrals, and your relationship with carriers.

"Educate your clients and you'll never have to sell them a thing. Stop trying to recommend what you think they want. Get curious, find the pain point, and when you solve it, they already sold themselves." – Brent Crawley, The Premier Agency

The through-line across all five trends is the same: Medicare distribution is maturing. The agents who treated it like a growth game are recalibrating. The ones who built for quality, retention, and relationships from the start are positioned to win.

We'll be sharing more from Medicarians in the coming weeks. If you want to see how Spark helps agencies put these ideas into practice, book a demo.

.jpeg)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.jpeg)